New investment in wood processing spotlights future log supply

Across the country new investment is either confirmed or signalled for upgrading processing mills and manufacturing plants. This is good news for the forest industry and essential to realising the New Zealand Wood Council’s (WoodCo) ‘$12 billion by 2022’ export goal. Processing more logs onshore, at least 70% compared to the present 45-50%, is a key element in achieving this target. The upgrade and expansion announcements do not mean it is plain sailing for mills to catch-up on deferred maintenance and capex investment, however it does confirm that solid wood and pulp processors see a good future in New Zealand and their belief they can be internationally competitive.

In the central North Island, Rotorua-based Red Stag has confirmed they will construct a state-of-the-art super mill which will double log input to 1.2+ million cubic metres per year and increase output from 450,000 to 700,000 million cubic metres per year. Nearby, Oji Holdings, who with their 40% co-investor the Innovation Network Corporation of Japan (INCJ) have acquired Carter Holt Harvey’s Kinleith and Tasman (Kawerau) mills, are expected to undertake a mill modernisation programme that will increase their need for wood fibre.

Developments at Kawerau include Sequal Lumber’s installation of geothermal drying kilns, which will enable them to double their mill output. Closed former mill sites are also being reappraised, for example, the Tachikawa mill site in Rotorua has been purchased by investors with plans to re-establish a sawmill. In Taupo, Pacific T&R’s new high-tech plant to produce terpenes and rosin from radiata pine stumps is due for commissioning in early 2015; and new firm Carbon Producers Limited is being established to make carbon activated products from forest biomass and other plant sources. The latter examples will allow value to be recovered from more of the forest biomass.

Elsewhere, Pan Pac Forest Products Limited (Pan Pac) purchased the former Southern Cross Forest Products Limited (in receivership) sawmilling and drying assets at Milburn and Milton in November. Following upgrading of both sites, full production is expected from April 2015, regenerating local jobs. Regional mills in Taranaki, Auckland and Northland are also modernising their plant to improve efficiency and worker safety, and lift product quality and diversity. Other investors are exploring how they can utilise New Zealand’s renewable forest resource, relative abundance of clean energy and water, trade agreements and stable political situation.

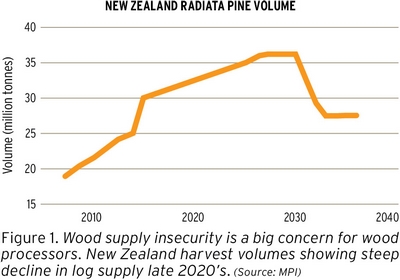

These developments highlight the importance of replanting existing forests and farm woodlots, and establishing new forests. New Zealand’s future wood supply curve is well-known (Figure 1) and shows that while the harvest has scope to increase to 33-35 million cubic metres over the next decade (last year the harvest was a record 30 million cubic metres), more log supply will be required from the late 2020s.

Increasing the security of future log supply has many positive corollary benefits. Tree planting and forest silviculture generates employment; contributes to reduced nutrient leaching and increased biodiversity; and, in light of new global efforts to address the threats posed by climate change, will help lower New Zealand’s greenhouse gas emissions.

Learnings from the 1990s planting boom indicate we need to think carefully about where forests are planted (e.g. future harvesting and transport costs, likely future wind and fire risk); the optimum tree genetics and establishment methods for a site, the use and integration of other species with commercial value (e.g. co-crops such as manuka and ginseng), and payments for a wider range of forest ecosystem services (e.g. payments for carbon storage and/or purchase nitrogen discharge allowances).

Establishment costs can be assisted through payments for carbon, Afforestation Grants and other commercial arrangements, but also through consideration of alternative forest systems with, for example, shorter rotations and higher planting rates.

Scion is heavily engaged with forest growers and mill owners in developing the knowledge and technology necessary to secure a future supply of wood, wood fibre and other forest biomass that will meet processor and market requirements. The stimulus provided by new investment in wood processing and value-added manufacturing using materials from forests bodes well for the forest industry’s ongoing significant and multi-faceted contribution to the New Zealand economy.

I welcome any comments you might have on this topic or on any of the other articles featured in this edition of Scion Connections. On behalf of the Scion Board and staff, we extend our best wishes to you, your family and friends for Christmas and a fruitful 2015 year.

Dr Warren Parker

Chief Executive